The construction of a socio-cultural narrative is one of the fundamental building blocks on which political projects are built. President Alberto Fernández, in charge of an eclectic pan-Peronist coalition that spans all the way from the left to the right, has struggled to find his origin myth and the accompanying mythology, beyond relying on the traditional Peronist fables, yet one of his recurring points is to blame the Mauricio Macri administration for the country’s evils, among them excessive indebtedness. As with most thorny issues in Argentina, it’s interesting that Alberto’s story, which is also one of the only areas in which he is completely in tune with Vice-President Cristina Fernández de Kirchner, masks the fact that both Peronist leaders also sunk the country deeper in debt during their own tenures. In other words, the country’s reckless borrowing didn’t begin with Macri, but with Cristina, and endures even today, with Alberto. Macri did clearly make the problem a lot worse, but all three are guilty.

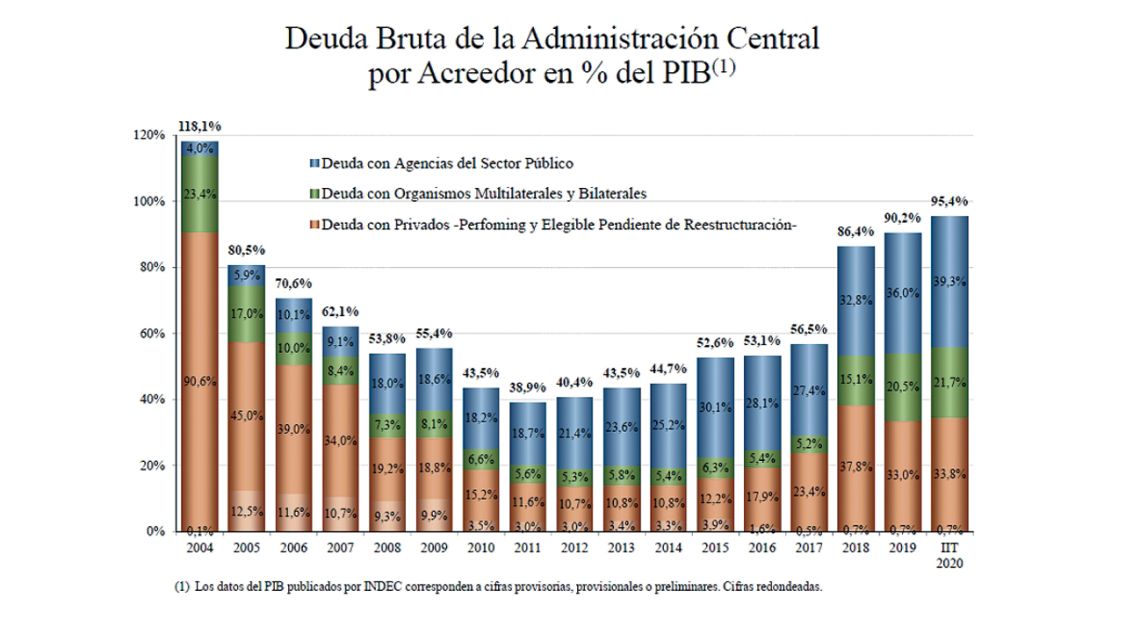

According to the latest figures published by the Finance Secretary, in Alberto Fernández’s 11 months in power through to October the central government’s gross debt rose by US$19.8 billion to US$333.1 billion. Taken over the first six months of the year, debt to GDP has risen to 95.4 percent, an indicator that has been on the rise since 2012 during the early days of Fernández de Kirchner’s second mandate. Of that debt, nearly 80 percent is in foreign currency while some 41 percent is owed to other entities within the Argentine state.

Economy Minister Martín Guzmán was brought in from Columbia University in order to restructure the country’s massive sovereign debt pile, much of which was accumulated under the Macri administration. One of President Fernández and Veep Cristina’s battle cries throughout their electoral campaign and their first 11 months as the Executive has been to blame Macri for destroying the Argentine economy but putting the interests of the financial sector before the people, liberalising currency markets to allow for foreign asset formation (ie. dollar buying), which then fuelled capital flight. The sovereign, the argued, took unnecessary and negligent risk by taking on unsustainable amounts of debt, leaving them with a heavy burden in their quest to “put Argentina back on its feet.” Macri and his economic team, including former finance secretary and Central Bank President Luis “Toto” Caputo, were only able to do this because CFK left them a public administration that had a very low debt to GDP ratio.

In order to present a coherent economic plan, Guzmán and Alberto needed to restructure the sovereign debt with private creditors (something that has already been achieved) and then complete negotiations with the International Monetary Fund (a process that is currently underway) that irresponsibly lent Macri US$44 billion, the official narrative says. IMF chief Kristalina Georgieva was asked in a letter signed by Senators from the ruling Frente de Todos coalition responding to Cristina to take responsibility for the billions it helped Macri’s friends fly out of the country, and to avoid putting strict conditionality under a new programme in order to let the country grow. In response, the opposition Juntos por el Cambio coalition indicated that Macri had to borrow to cover the massive fiscal deficit left behind by Cristina.

The accompanying chart to this article is quite explicit, showing how Néstor Kirchner managed to aggressively reduce Argentina’s debt burden through the 2005 sovereign debt restructuring with private creditors, the down payment to the IMF that same year, and the smaller but important 2010 restructuring led by then-economy minister Amado Boudou. Starting in 2011, Cristina began to aggressively expand the country’s debt, only it wasn’t with the private sector and in dollars, but with its own public sector. Starting early on, the Kirchners knew of the importance of owning and controlling the different “cajas” or funds available to the state. Néstor though had the advantage of a commodities super-cycle that saw the price of soybeans spike to record highs, growing four-fold from the 2000s to the 2012 peak.

The global financial crisis that began when Lehman Brothers went bust precipitated the beginning of the end of that trend, and with it Argentina’s dual surpluses (trade and fiscal), forcing the Ks to look for more “cajas.” They nationalised the private pension system, known by the signals AFJP, nationalised oil giant YPF, and sought to pay debt with Central Bank reserves. With the commodities super-cycle exhausted, Mrs. Fernández de Kirchner took debt-to-GDP from 38.9 percent in 2011 to 52.6 percent by the end of her second mandate in 2015 (Néstor passed away in 2010). The vast majority of that debt was intra-government debt, as Cristina was effectively locked out of capital markets given outstanding creditors who didn’t accept Néstor’s restructurings, including billionaire hedge fund manager Paul Singer who was the engine behind the famous “pari passu” judgment by Judge Thomas Griesa in New York. Thus, intra-government debt went from 18.7 percent by the end of 2011 — the starting point of Cristina’s second mandate — to 30.1 percent when she handed over the presidency to Macri. In her first term in office (2007 to 2011), she doubled debt with public sector agencies from 9.1 percent to 18.7 percent of gross debt.

Macri’s original plan was to stop the incestuous inter-government debt used by Cristina to finance ever-growing fiscal deficits and replace it by private sector debt. The theory was that a shock of confidence would result in private sector lending and foreign investment, allowing Argentina to rollover its debt as normal countries do. In his first two years in office, Macri settled with holdout creditors and once again took to private borrowing, reducing the weight of intra-government debt while taking private creditors’ share of the outstanding debt from 12.2 percent to 23.4 percent, including the (in)famous century bond. That’s when things got hairy.

Despite an initial devaluation, Macri did gain the trust of the private sector, at least international credit markets, which lent him money recklessly. By the end of 2017 he had won midterm elections that seemed to bury Cristina’s political dreams of making a comeback, lowering inflation while generating GDP growth. But firing Federico Sturzenneger from the Central Bank, acknowledging higher inflation rates, and a political battle with the Peronist opposition that eroded Macri’s control of the socio-political situation, set him up for what came later: a global run on emerging markets in 2018 that castigated Argentina. And despite claiming he would take on much needed reforms, he continued expanding the fiscal deficit.

Debt-to-GDP surged to 90.2 percent by the end of 2019, with a string of devaluations and an IMF bailout gone bad. Rampant inflation, three out of four years in a recession, and the same problems we’ve always had: Macri’s presidency and his economic policy in particular was an absolute failure.

Argentina’s “external restriction” has been a persistent problem for much of the 20th century. Today’s bi-monetarism is a consequence of the state’s incapacity to finance itself effectively, which in turn is directly caused by the Argentine political class’ incompetence, translated into “lack of confidence” by the market. Macri blew his chance to restructure the state and its financial relationships with itself, productive actors and foreign creditors. Alberto Fernández claims he’s trying to do that with Economy Minister Guzmán’s orthodox pivot, but that has been pushed to the background by the “wealth tax” and the debate about the legalisation of abortion.

Obviously, the global coronavirus pandemic changes everything. It is still too early to tell which path Alberto will lead us down.

Comments