Argentina may be in deep financial trouble but its Central Bank is comfortably back in the black – thanks to a small accounting manoeuvre.

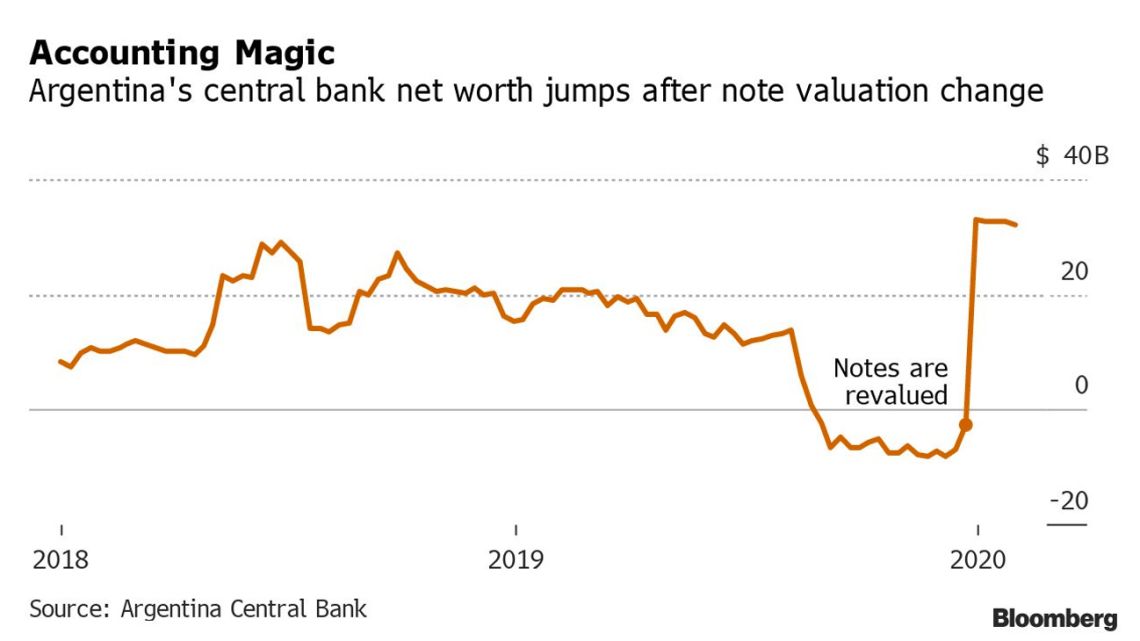

A little-noticed decision by policy-makers late last year to change the way they value government bond holdings transformed the Central Bank’s balance sheet overnight, turning what had been a net worth of minus US$2 billion into plus US$33 billion.

Officials have made little effort to explain the move – they just say it’s part of a wide-ranging emergency law to shore up the economy – but analysts note how it will pave the way for the bank to start turning over dividends to the cash-strapped government.

“Today it’s lying about its profits in order to print money, finance the government and make itself even more insolvent,” said Aldo Abram, economist at Buenos Aires-based Libertad y Progreso, a research centre that advocates for free markets.

These sorts of payments are commonplace in many parts of the world – including in Argentina, where US$44 billion in dividends were transferred to Treasury coffers over the past decade – but by pumping pesos into a fragile economy they would threaten to add to a surge in consumer prices that has already pushed the country’s inflation rate over 50 percent. What’s more, the bond valuation manoueuvre rekindles old questions about the trustworthiness of Argentina’s book-keeping at a time when it’s trying to preserve reserves and preparing to begin debt restructuring talks with local and foreign creditors.

Among those creditors is the International Monetary Fund, which had insisted that the government square up on its old debts with the Central Bank as a key condition of a US$56-billion loan package it gave the country back in 2018. IMF officials met this week in Buenos Aires with top economic aides to President Alberto Fernández.

It was an emergency law passed in the early days of Fernandez’s government that had allowed the Central Bank to make the accounting change.

Officials then marked up the value of some peso-denominated government bonds, known as “non-transferable notes,” in the bank’s portfolio to par. Previously they had been assigned a value based roughly on the steep discounts that similar government debt was trading at in the local market. The move boosted the recorded value of the bonds to 360 billion pesos (US$5.9 billion) from 251 billion pesos.

“To log these bonds at par value is a scam, a hoax,” Abram said.

A spokesman for the Central Bank declined to comment for this story. When asked about the valuation change in a January interview, Central Bank chief Miguel Pesce said he wasn’t concerned with analyst debates on how the notes should be valued because he expected the bank to hold the notes through maturity.

CHANGES, CHANGES

In Argentina, a country which has been hit by frequent financial crises, repeated changes in the way the Central Bank operates are common. The institution has had 62 presidents since its foundation almost 85 years ago and isn’t, officially or in practice, independent from the government. Its charter has been modified 11 times in almost three decades.

Approved in 2012 under the presidency of current vice-president Cristina Fernández de Kirchner, it states that the institution is automatically forced to send the government all earnings after they hit a certain threshold.

The notes that the Central Bank revalued were originally issued in 2005 by the government to raise hard currency to pay back an IMF loan. The obligations have been continually rolled over since then.

When the Fund returned to the country in 2018, granting Argentina its biggest-ever loan, one of the conditions it set was that the Central Bank should value these notes at market prices as a way of having a more accurate balance sheet.

Given that their market value is significantly lower than parity, this put the Central Bank’s net worth in the red for the latter months of 2019.

“These notes are an asset that won’t be available in case of a liquidity crisis such as currency run or a debt crunch,” said Martin Vauthier, an economist at Buenos Aires-based consultancy Eco Go SA. “It’d be more realistic and reasonable to consider them at market value.”

In addition to allowing the change in valuation, the economic emergency law passed in December authorised the Treasury to borrow as much as US$4.6 billion from the bank through non-transferable notes.

Argentina drew that entire amount in the first two weeks of January. That was done so that the government could pay for the interest on its dollar debt without using funds from the Treasury, Economy Minister Martín Guzmán said in a February 12 presentation to Congress.

“Using the Treasury cash buffer would have meant real austerity at a time of recession, which would be very harmful,” Guzmán said. “Argentine society is making an effort by paying debt with reserves. It can’t last long.”

The Central Bank has a total stock of US$51.3 billion of these non-transferable notes, including the ones from those January transfers. Most of them mature between 2021 and 2025, according to data compiled by the Argentine Institute of Fiscal Analysis. The government will owe the bank more than US$10 billion of capital and interest accrued for these notes in 2021 alone. They could also be rolled over.

At a time when Argentina is locked out of debt markets, “it’s inaccurate to value these notes as if the government were going to pay you in 10 years,” said Bruno Panighel, an economist of the Argentine Institute of Fiscal Analysis.

related news

by IGNACIO OLIVERA DOLL, Bloomberg

Comments