A fresh breeze is cutting through the dysfunctional miasma that envelops Argentina’s economy these days — and it’s coming from the country’s oil and gas industry, of all places.

Powered by a large shale deposit in Patagonia, oil production is increasing at a double-digit rate, companies buzz with new projects to boost exports and natural gas output and industry executives are looking ahead to the upcoming presidential election with high hopes for an improved business environment. Some of the stocks most exposed to Argentina’s hydrocarbon business, such as national champion YPF SA and pipeline operator Transportadora Gas del Norte SA, are up more than 300 percent in dollar terms in the past 12 months. The start of a new, 573-kilometre (356-mile) gas pipeline is also expected to save billions in energy imports, one of the biggest policy headaches of recent administrations.

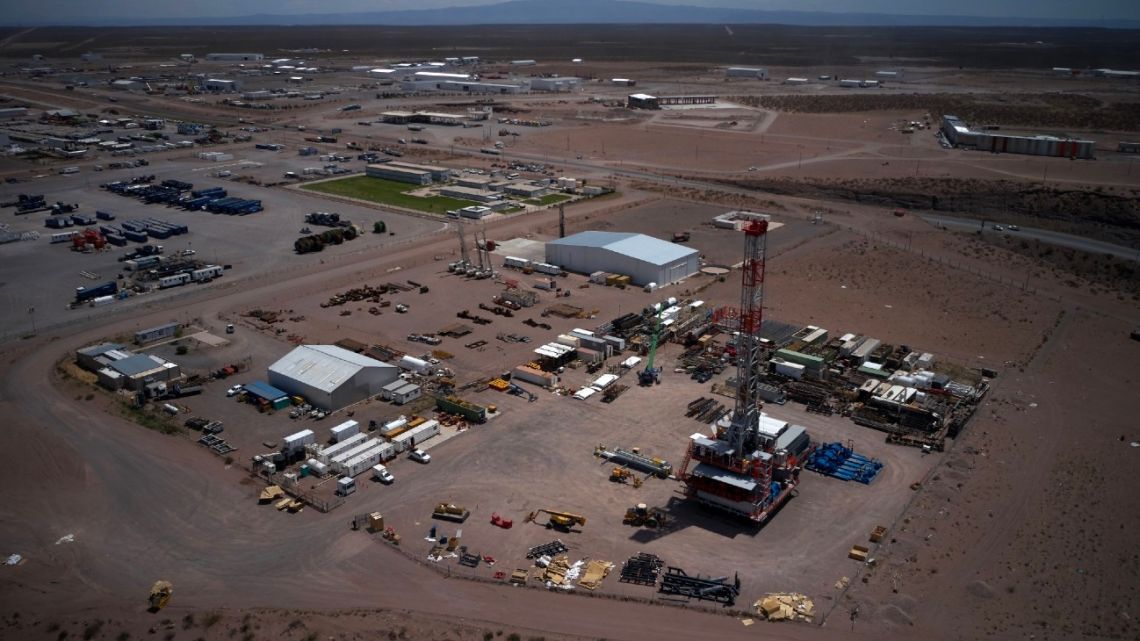

Thanks to well productivity that outstrips even its US shale counterparts, the Vaca Muerta (or “Dead Cow”) patch in Neuquén Province could reach one million barrels per day of oil production by decade’s end, according to a report by consultancy firm Rystad Energy. If that explosive growth happens — and it’s a big “if” — Argentina could find itself back on a path toward energy self-sufficiency, boosting much-needed dollar reserves by exporting most of the light crude added with the extra capacity.

“This is absolutely a once-in-a-generation opportunity,” says Alexandre Ramos-Peon, head of shale research at the firm. “Either it happens now, or they are going to miss the boat. At some point the world will have no need for this oil.”

Now this is Argentina, the heartland of political volatility and economic mismanagement, where a lot of things can go horribly wrong. In fact, the industry has been operating under difficult regulatory and economic conditions for the past two decades; the Vaca Muerta boom should have happened much sooner.

Capital controls and multiple exchange rates complicate the development of a solid supply chain and oil services network. High financing costs or lack of access to international markets altogether diminish private investment opportunities. The government has tended to cap crude exports and domestic gasoline prices to privilege the local market, shielding consumers from higher international prices at the cost of limiting shipments and discouraging new investments.

Yet despite all these challenges, and with the help of some ad hoc policies to try to bypass them, the industry is probably in its best position in years. As a result, oil executives are growing more confident that whoever wins the October election “won’t try to kill the golden goose,” says Paulo Farina, a Buenos Aires-based consultant and former energy official. “The political consensus is that the strong pace that the sector is gaining shouldn’t be interrupted,” Farina says.

The next Argentine government is likely to be more business-friendly than the current Peronist left-wing coalition. Notwithstanding some internal differences, the opposition coalition that leads the polls is seen as supportive of the industry. Both its candidates visited the Vaca Muerta project in the past year. But even if the Peronist candidate Sergio Massa achieves a surprise win, his track record as economy minister suggests that he also is close to the oil companies.

A devaluation of the peso anticipated during the first year of whatever government that takes power on December 10 will certainly shake up things for corporates. The expectation is that after the first shock, a more straightforward macro approach will deliver improvements in the economy, the business environment and credit access. It could also convince the oil majors currently on the ground, including Shell Plc and Chevron Corp, to bet bigger on Argentina. It may even give renewed force to some of the country’s more ambitious projects, including offshore exploration and LNG production designed to fill the gap left by Russia’s displacement from the market following its invasion of Ukraine.

Argentina has a long history with oil and gas exploration, first finding crude in the country’s south more than a century ago. It once produced more oil than Brazil (today, Brazil produces about five times more than its southern neighbour). But macroeconomic instability, energy nationalism and policy zigzags — privatising YPF, only to then nationalise it again 13 years later — greatly curtailed the industry’s potential.

Now geology, technology and even geopolitics are opening a new opportunity for Argentina before hydrocarbon demand peaks. Let’s hope the country’s politicians don’t blow it.

related news

by Juan Pablo Spinetto, Bloomberg

Comments