In the 99 years since it was founded to pump the oil fields of Patagonia, Argentina’s energy driller YPF SA has been whipsawed by countless booms and busts. If global oil markets weren’t collapsing, it seemed, then Argentina was mired in a debt crisis that was wreaking havoc on the whole nation’s finances.

Never, though, had the company been pushed into a large-scale default of any kind. Until, it would appear, now. Word of this came in an odd way: officials at state-run YPF sent a press release in the dead of night laying out a plan to saddle creditors with losses in a debt exchange.

Implicit in its statement was a threat that traders immediately understood – failure to reach a restructuring deal could lead to a flat-out suspension of debt payments – and they began frantically unloading the shale driller’s bonds the next morning. Some two weeks later, the securities trade as low as 56 cents on the dollar.

Creditors, including BlackRock Inc and Howard Marks’s Oaktree Capital Group, are gearing up for bare-knuckled negotiations just four months after ironing out a restructuring deal with the government that marked the country’s third sovereign default this century alone.

YPF’s downfall underscores just how hard the pandemic has hammered both the global oil industry and the perennially hobbled Argentine economy. Dollars are now so scarce in Buenos Aires that the Central Bank refused to let YPF buy the full amount it needed to pay notes coming due in March. That was the immediate cause of the restructuring announcement.

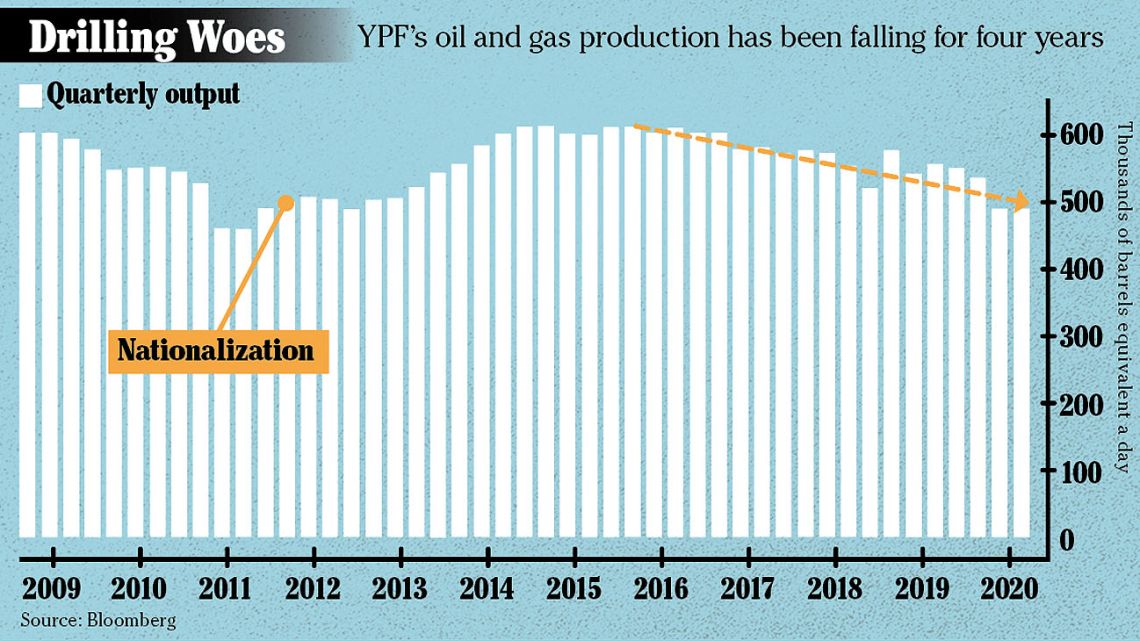

A longer view reveals a steady decline in the company’s finances since the government re-nationalised it in 2012 and forced it to swell payrolls, artificially hold down domestic fuel prices and skimp on investments, leading to four straight years of oil-and-gas output declines.

In order

YPF must now reach a deal with creditors to get its finances in order to boost investment in the gas-rich Vaca Muerta shale formation in Patagonia.

The task is even more urgent as the South American winter approaches with YPF unable to meet domestic gas demand, meaning Argentina will have to boost imports – and fork over precious hard currency – in the middle of a global spike in prices.

“The Central Bank’s decision really put YPF between a rock and a hard place,” said Lorena Reich, a corporate-debt analyst at Lucror Analytics in Buenos Aires.

In private conversations with investors, YPF officials are portraying the deal as a voluntary exchange and are insisting that they will pay back all their bonds – with the exception of the notes coming due in March – whether they are tendered in the swap or not. But that’s certainly not how investors interpret the situation, and ratings companies say the proposal constitutes a distressed exchange that would be tantamount to default.

The company’s US$413 million in bonds due in March tumbled 6.5 cents Tuesday, the most since September, to about 82 cents on the dollar.

Overall, YPF is seeking to restructure US$6.2 billion of bonds, pushing back a total of US$2.1 billion in debt payments through the end of next year so that it can invest the money in bolstering production. The deal offers investors a slight upside from current bond prices, but would stick creditors with losses of as high as 16 percent on a net-present-value basis, according to calculations by Portfolio Personal Inversiones, a local brokerage.

While some investors had anticipated YPF would try to refinance its short-term debt – without imposing any losses – the plan to restructure virtually all the company’s overseas bonds was a big surprise.

“The offer crossed the line of reason,” said Ray Zucaro, the chief investment officer at RVX Asset Management in Miami, who owns YPF bonds. “There was no reason they needed to include all the bonds when they only needed relief on the short-dated notes.”

YPF says it included all its securities in the swap to give all its bondholders a fair shot at exchanging into a new export-backed note maturing in 2026 that offers more protection than unsecured debt.

Creditors have begun to form groups to negotiate the terms of the restructuring, and while the talks haven’t begun in earnest, the company says it’s willing to negotiate. On January 14, YPF amended some of the rules for its consent solicitation after investor outcry over a procedural issue.

Cash crunch

Argentina’s cash crunch couldn’t come at a worse time for YPF, which was already facing a drop in demand because of the pandemic.

The driller needs more investment to ramp up capital-intensive shale production in Vaca Muerta as ageing traditional fields decline. It’s expected to spend US$2.2 billion in 2021 after last year’s paltry US$1.5 billion. But that’s still a far cry from the more than US$6 billion a year it invested in the wake of the nationalisation.

As the company looks for savings in the bond market, it’s also slashing other costs, cutting salaries and reducing its bloated workforce by 12 percent. It’s trying to sell stakes in some oil fields, as well as its headquarters in Buenos Aires, a sleek glass skyscraper where executives take calls looking out over the vast Río de la Plata estuary into Uruguay.

Founded in 1922 as one of the world’s first entirely state-run oil companies, YPF was passed from nationalist governments to military dictatorships until the early 1990s, when it was sold to Madrid-based Repsol SA as part of a short-lived attempt to free up the economy. In 2012, President Cristina Fernández de Kirchner’s government expropriated 51 percent of the company, eventually paying Repsol US$5 billion in bonds for its stake. YPF’s market value today is just US$1.6 billion.

The Central Bank’s refusal to sell YPF the dollars it needs to pay its obligations, despite the company’s earlier efforts to refinance its short-term debt, is a bad sign for all overseas corporate bonds from Argentina, according to the financial services firm TPCG. The concern is that if the country’s flagship company isn’t eligible to buy dollars at the official exchange rate as the bank seeks to hold onto hard-currency reserves, no one else will be either.

“The Central Bank’s message is pretty clear,” said Santiago Barros Moss, a TPCG analyst in Buenos Aires. “There just aren’t enough dollars in Argentina for corporates right now.”

by Scott Squires & Jonathan Gilbert, Bloomberg

Comments